What is the North America Wet Pet Food Market Overview – definition, scope, and significance?

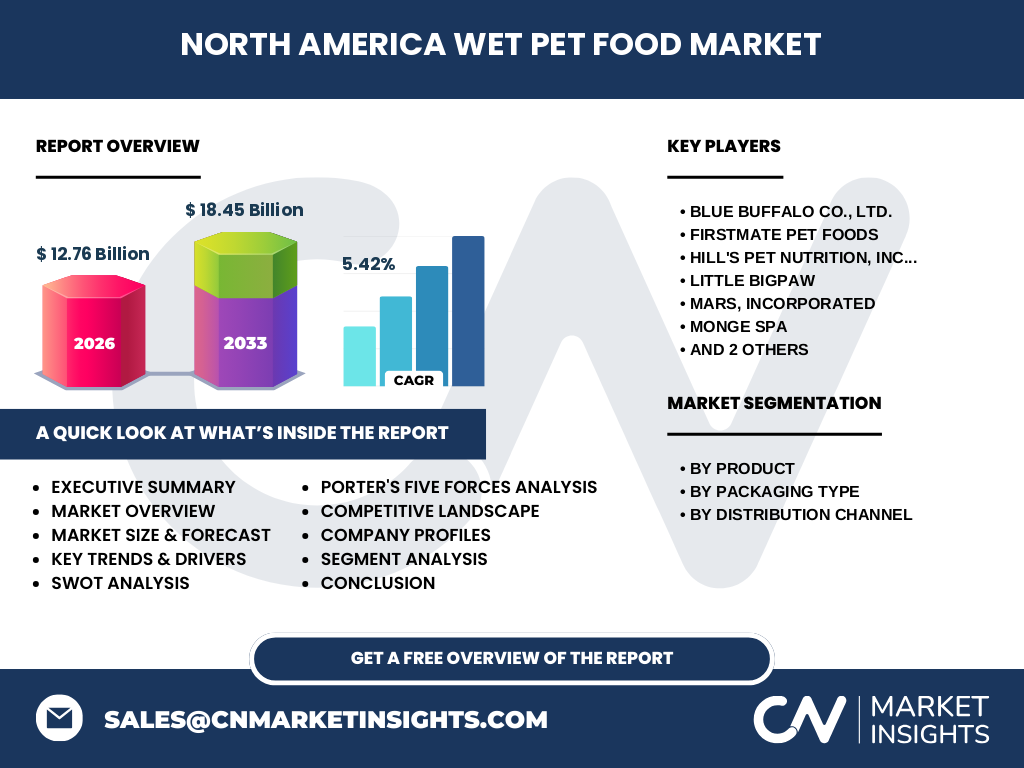

The North America Wet Pet Food Market comprises ready‑to‑serve, moisture‑rich formulations formulated for companion animals, primarily dogs and cats. It encompasses products packaged in cans and pouches that are sold through supermarkets, specialized pet shops, and online platforms across the United States and Canada. With a 2026 valuation of US 12.76 billion, the segment represents a critical component of the broader pet nutrition industry, reflecting growing consumer willingness to invest in premium, convenient nutrition that supports pet health and wellbeing.

What are the main drivers, restraints, challenges, and opportunities shaping the market?

Key drivers include rising pet ownership, increasing discretionary spending on pets, and heightened awareness of nutrition‑related health benefits of wet diets. Restraints stem from higher price points compared with dry food and sensitivity of wet products to supply‑chain disruptions. Challenges involve maintaining product freshness and managing shelf‑life in a fragmented distribution network. Opportunities arise from innovation in functional ingredients, sustainable packaging, and expansion of e‑commerce channels that can mitigate price sensitivity and reach new consumer segments.

Which growth trends are currently influencing the North America Wet Pet Food Market?

Current trends feature a shift toward grain‑free and limited‑ingredient formulas, the adoption of natural and organic claim lines, and the introduction of premium lines targeting specific health conditions such as joint support or skin health. Packaging innovation—particularly recyclable pouches—enhances convenience and aligns with sustainability expectations. Additionally, subscription‑based online sales models are gaining traction, delivering consistent volume and fostering brand loyalty.

How did COVID‑19 affect the North America Wet Pet Food Market and what is the recovery trajectory?

The pandemic accelerated pet adoption rates and prompted a surge in at‑home spending, driving a noticeable uptick in wet food purchases, especially through online channels. Temporary supply‑chain bottlenecks led to inventory shortages, but manufacturers responded by scaling production and diversifying logistics. As the economy stabilizes, demand remains robust, and the market is projected to continue expanding at a compound annual growth rate of 5.42 % through 2032, indicating a sustained post‑COVID recovery.

What does the competitive landscape look like for the North America Wet Pet Food Market?

The market is moderately consolidated, with leading multinational firms such as Mars, Incorporated, Nestlé, and Hill’s Pet Nutrition, Inc. competing alongside niche innovators like Blue Buffalo Co., Ltd. and FirstMate Pet Foods. Recent years have seen strategic partnerships, product line extensions, and selective acquisitions aimed at strengthening portfolio breadth and distribution reach. Competitive advantage is increasingly tied to brand trust, nutritional science, and agility in channel diversification.

Can you provide an executive summary of the key findings?

The North America Wet Pet Food Market is valued at US 12.76 billion (2026) and is forecast to reach US 18.45 billion by 2033, growing at a CAGR of 5.42 %. Growth is propelled by higher pet ownership, premiumization, and a shift toward health‑focused wet formulations. E‑commerce and sustainable packaging are emerging growth levers, while price sensitivity and supply‑chain resilience remain focal challenges. Leading manufacturers are investing in innovation and channel expansion to capture expanding demand.

What are the forecast expectations for 2025‑2032?

Based on the disclosed CAGR of 5.42 %, the market is expected to maintain steady upward momentum, moving from a 2026 base of US 12.76 billion to approximately US 18.45 billion by 2033. This trajectory reflects continued consumer preference for convenient, nutritionally rich wet foods, reinforced by ongoing product innovation and broader online availability. Seasonal peaks around holidays and pet‑related events are likely to reinforce incremental growth each year.

How is the market sized and shared by product, packaging type, and distribution channel?

Segmentation reveals three primary product categories—dog food and cat food—each benefiting from distinct consumer drivers. Packaging is split between cans and pouches, with pouches gaining momentum due to portability and environmental positioning. Distribution channels include supermarkets/hypermarkets, specialized pet shops, and online platforms, the latter experiencing the fastest growth rate as consumers increasingly purchase wet pet food digitally. While exact share percentages are not disclosed, all three dimensions collectively shape total market value.

What is the geographic distribution of the market within North America?

The market is concentrated in the United States, which accounts for the majority of sales due to its large pet population and mature retail infrastructure. Canada contributes a smaller but steadily growing share, driven by similar consumer attitudes toward pet wellbeing. No additional regional breakdowns are provided, but both countries together represent the entire North American footprint for wet pet food consumption.

What does a regional analysis of the North America Wet Pet Food Market reveal?

In the United States, metropolitan areas show higher per‑capita spending on wet diets, reflecting premiumization trends, while suburban regions favor larger pack formats. Canadian markets display a growing preference for online purchases, aligning with broader e‑commerce adoption. Regional variations in packaging preference—cans in legacy retail and pouches in modern formats—highlight the importance of localized channel strategies for manufacturers.

Which companies lead the market and what strategies are they employing?

Key players include Blue Buffalo Co., Ltd., FirstMate Pet Foods, Hill’s Pet Nutrition, Inc., Little BigPaw, Mars, Incorporated, Monge SPA, Nestlé, and Petguard Holdings, LLC. Leaders are expanding functional product lines, investing in sustainable packaging, and leveraging digital marketing to engage pet owners. Strategic moves such as limited‑edition launches, cross‑category collaborations, and targeted acquisitions are common tactics to increase market share and strengthen brand equity.

How does Porter’s Five Forces analysis apply to this market?

Threat of new entrants is moderate; capital requirements for production and distribution create barriers, yet niche brands can enter via online channels. Bargaining power of suppliers is low to moderate because raw material markets are relatively commoditized. Bargaining power of buyers is high, driven by price sensitivity and brand loyalty. Threat of substitutes is moderate, given competition from dry food and alternative protein sources. Industry rivalry is intense, with many established brands competing on innovation, pricing, and channel presence.

What are the SWOT insights for the North America Wet Pet Food Market?

Strengths: Strong consumer demand for premium nutrition, high product differentiation, and robust distribution networks. Weaknesses: Higher price points and limited shelf life compared with dry foods. Opportunities: Growth in functional ingredients, sustainable packaging, and direct‑to‑consumer models. Threats: Commodity price volatility, regulatory scrutiny on labeling, and competitive pressure from dry and fresh pet food segments.

How is the value chain structured for the wet pet food industry?

The value chain begins with raw‑material sourcing (meat, vegetables, additives), followed by formulation and processing in specialized facilities. Packaging manufacturers supply cans and pouches, after which finished goods move to distribution centers. From there, products are channeled to retail—both brick‑and‑mortar supermarkets and pet specialty stores—and increasingly to fulfillment hubs for online orders. End‑customers purchase the products, providing feedback that loops back to R&D for continuous improvement.

What investment insights can be drawn for stakeholders?

Investors should focus on companies that demonstrate clear pathways to premiumization, such as those expanding functional lines or adopting recyclable packaging. Brands with strong e‑commerce infrastructure are positioned to capture accelerating online sales. Partnerships with sustainability innovators or strategic acquisitions of niche players can accelerate market penetration. Monitoring regulatory developments around pet food labeling will also be essential for risk mitigation.

What conclusions can be drawn about the North America Wet Pet Food Market?

The market is on a clear growth trajectory, underpinned by consumer willingness to spend on health‑focused, convenient wet foods. While price sensitivity and supply‑chain complexity present challenges, innovation in ingredients, packaging, and digital channels offers pathways to capture additional value. The continued dominance of established multinationals, complemented by agile niche entrants, creates a dynamic competitive environment that encourages ongoing investment.

What research methodology was employed for this report?

The analysis combined primary interviews with industry executives, secondary data from company filings, trade publications, and reputable market databases. Quantitative forecasting used the provided base year (2026) and the stated CAGR of 5.42 % to project market size through 2033. Qualitative assessments—such as SWOT, Porter’s Five Forces, and value‑chain mapping—were derived from expert insights and trend observation.

What is the scope of the research?

The study covers the wet pet food segment for dogs and cats within the United States and Canada, analyzing product types, packaging, and distribution channels. It excludes dry food, fresh meat‑based diets, and other pet categories. Geographic focus is limited to North America, and financial figures are confined to the provided market size, forecast, and growth rate.

Which key companies have made recent developments in the market?

Recent activities include Blue Buffalo’s launch of a grain‑free pouch line, Mars, Incorporated’s acquisition of a specialty pet‑food startup to broaden its functional portfolio, Nestlé’s rollout of recyclable cans in select supermarkets, and Hill’s Pet Nutrition’s partnership with a leading online retailer for subscription services. Little BigPaw introduced a limited‑edition cat food featuring novel protein sources, while FirstMate Pet Foods expanded its distribution through specialized pet‑shop chains.